🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

Is Burial Insurance Worth It? | Memorials.com Info Center

🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Largest Funeral Retailer Online📦Over 50,000 products🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

Most people haven’t made any financial plans for their funerals, although funeral services today cost thousands of dollars. This implies that your end-of-life expenses must be borne by your devastated family and friends.

Fortunately, people can make provisions for the financing of their funerals by taking out funeral insurance. This article explains all you should know about burial insurance and why you should get one.

What is funeral insurance?

Funeral insurance, commonly referred to as “last expense insurance,” is a kind of whole life insurance policy made to pay for funerals, burials, and other end-of-life costs. Due to the high cost of funerals, buying funeral insurance might help your family pay for any costs they have to pay after you die.

Burial insurance has a death payout of $5,000 to $25,000, and you can purchase this insurance without a medical exam after completing a few health-related application questions.

This insurance type isn’t designed for people who are raising children and need a life policy to pay for larger responsibilities, like kids’ college tuition, mortgage, or income replacement throughout their peak working years.

It’s targeted at people on limited incomes and perhaps in poor health, whose families may not have any money or any life insurance policy to pay their funeral expenses.

What funeral insurance isn’t?

As opposed to the standard term life, universal life, and whole life policies, funeral life insurance is created expressly to cover one-time and transient costs. It isn’t intended to serve as a source of income or to pay for significant expenses like a home or college. It’s also not a form of investment or retirement plan.

Although its main purpose is to pay for funeral expenses, your beneficiary may also use it to pay for other end-of-life obligations, such as unpaid credit card debt, medical bills, or other bills accumulated in the month of your passing (utility bills, phone bills, car payment, etc.).

How does funeral insurance work?

Funeral insurance works similarly to typical whole life insurance. You simply need to decide who’ll be the beneficiary of your passing and the level of coverage you want. The beneficiary should get in touch with the insurance company to start the claims procedure as soon as possible after the insured’s passing. A claim form, a certified copy of the death certificate, and proof of identity may be requested from the beneficiary to access the payout.

Final Expense insurance has no limitations on how the payout may be used; it is intended to cover the costs your family members will incur in the event of your passing.

Your beneficiaries may decide to utilize the proceeds from your burial insurance for any of the following.

Due to the relatively lower coverage amount, your death benefit might not be much left over after your beneficiaries have paid for your final expenses.

If you want to leave behind a bigger amount of money, you should think about getting a policy that keeps more of its value, like a traditional whole-life policy.

The money is not legally required to be used for your funeral costs, so your family member is free to use it in any way they see fit.

Hence, you must pick someone who will manage this money according to your instructions when naming a beneficiary.

What is the cost of funeral insurance?

The typical funeral insurance plan offers $10,000 in coverage for around $50 per month on average, and just like regular insurance policies, the premiums can be paid every week or month.

The amount you end up paying a premium may be higher or lower depending on your gender, health, and whether you want more or less coverage. However, it’s typically a small round amount like $2 or $3 per week.

The death benefit the beneficiary gets is typically based on whatever that premium would buy given the insured’s present age. For example, a $3 weekly premium may provide a 36-year-old man with a $6,000 death benefit or a 9-year-old youngster with an $18,000 death benefit.

Why should you get funeral insurance?

It is easy to obtain.

You can purchase the coverage over the phone or online without having to undergo a medical examination. Candidates are questioned about their age, if they smoke, and whether they have any serious medical concerns.

Some insurance policies even guarantee acceptance without asking any medical-related questions. These are known as “guaranteed acceptance” or “guaranteed issue” life insurance policies and are created for those who are too ill to be eligible for other types of life insurance.

Guaranteed issue insurance doesn’t pay a death benefit for the first one, two, or even three years that the policy is in place. If they did, everybody would prefer to wait till they were close to passing away, pay one month’s worth of premiums, and have their beneficiaries receive $25,000.

No insurance company could continue to exist if they permitted this. The beneficiaries of the guaranteed policy, however, will get the premiums paid, plus interest, if the insured passes away while the waiting period is in effect.

It’s seemingly affordable.

While other whole life, term life, or guaranteed universal insurance plans may demand significantly higher minimum coverage levels of $50,000 or $100,000, burial insurance can be obtained for minor sums like $5,000 or $10,000.

But it can be hard to know if the prices for burial insurance are a good deal without getting quotes from more than one insurer that are customized and comparing prices.

A show of love

You can use burial insurance as a tool to assist your loved ones in covering your ultimate expenses. When you buy a burial insurance policy, your goal is to protect your loved ones from the burden of handling your final expenses.

No matter how you wish to be remembered, you can set aside some money for the last expenses like a casket or urn, memorial services, flowers, food, and a burial plot. This eliminates the need for your loved ones to cover these costs out of pocket.

Types of funeral insurance

Funeral insurance is a small whole life policy that’s frequently offered to senior citizens. The policies can be divided into two categories: simplified issues and guaranteed issues.

Simplified issue policies

This offers life insurance policy without a medical exam, but you must complete a health questionnaire. You may be refused coverage if you answer “yes” to certain questions, such as

Do you use a wheelchair?

Do you live in a nursing home?

Do you have a significant medical condition like diabetes, cancer, or heart disease?

Otherwise, you have a good chance of getting accepted, even as a senior.

Guaranteed issue policies

provide coverage without asking any questions and bypass the medical examination and health assessment. But guaranteed issue life insurance often costs more to account for the added risk because the insurers don’t know anything about the individual they’re insuring.

The drawback of these policies is that the death benefit of the insurance will typically be graded. Your beneficiaries will only receive a return of the premiums you paid, plus some interest, or a small portion of the insurance’s coverage value if you pass away within two or three years after purchasing the policy. But deaths that are unavoidable, like those caused by plane crashes, are often fully covered by the policy right away.

How are premiums for final expense insurance calculated?

There are four significant elements that affect the cost of burial insurance.

Age: The monthly charge will increase as you grow older when you purchase coverage.

Health: The price point is significantly influenced by your health. If you are in good health, there is no waiting period and you are eligible for a less expensive burial plan. Smokers in their senior years will pay higher premiums.

Gender: Men will have to pay more for insurance than women. There are several reasons behind this, but the main one is that women live on average four years longer than men do, which means that they will likely be contributing to the policy for a longer period.

Policy Amount: The more coverage you purchase, the higher your monthly cost will be. Costs will increase as coverage increases.

Does funeral insurance pay off?

Funeral insurance is frequently viewed as essential due to the rising cost of funerals and burials in our modern economy. The typical cost of a funeral can be as high as $15,000 to $20,000 depending on several factors.

The idea of having to come up with that amount of cash on short notice – especially after the deaths of young people or even healthy older people – might be as scary as a person can get in our hard-strapped, debt-burdened environment.

As such, it would be in the interests of people who worry that they would find themselves in such a situation or who worry that they might leave a family in such a dilemma to plan for it with burial insurance.

However, many experts caution that funeral insurance is not a good investment for the majority of families, especially those who have the means to cover these expenses. Some of the most vocal critics of the funeral insurance industry as a whole have even tried to pass laws that would make it hard to sell burial insurance policies or even ban them outright.

Expert opinion on funeral insurance

It is significant to highlight that, when purchased with caution, funeral insurance can be a good deal for customers, according to many professionals in the death care and financial industries.

Many experts will agree that burial insurance may be the ideal choice if a person is seeking a solution to ensure that his or her family is not burdened with the cost of a memorial ceremony or burial.

However, funeral insurance is nearly always detrimental to healthy, young people. These people would do well to make sure they have thoroughly investigated all their choices before making any life insurance purchases.

Customers should be fully aware that the individual selling to them has a stake in the sale, just like with any other financial product. So, it’s usually not a good idea to ask that person for advice unless the advice is backed up by a lot of independent research.

Sales representatives for burial insurance frequently cite the absence of a medical checkup as a selling point. This is because people, even healthy ones, don’t always like the idea of answering a bunch of annoying tests and questions that could be invasive.

As a result, even healthy individuals may be persuaded to purchase a burial policy for the same price as a much higher-yielding policy. Customers should keep in mind that getting a health exam can frequently result in a far better offer on life insurance.

Most consumer advocates won’t tell a client to buy burial insurance until at least one other traditional life insurance policy has been turned down.

(In actuality, we use the word “at least” with some caution. It is probably preferable, according to experts, to hold off on purchasing a burial insurance policy until after you have been declined by several life insurance firms.)

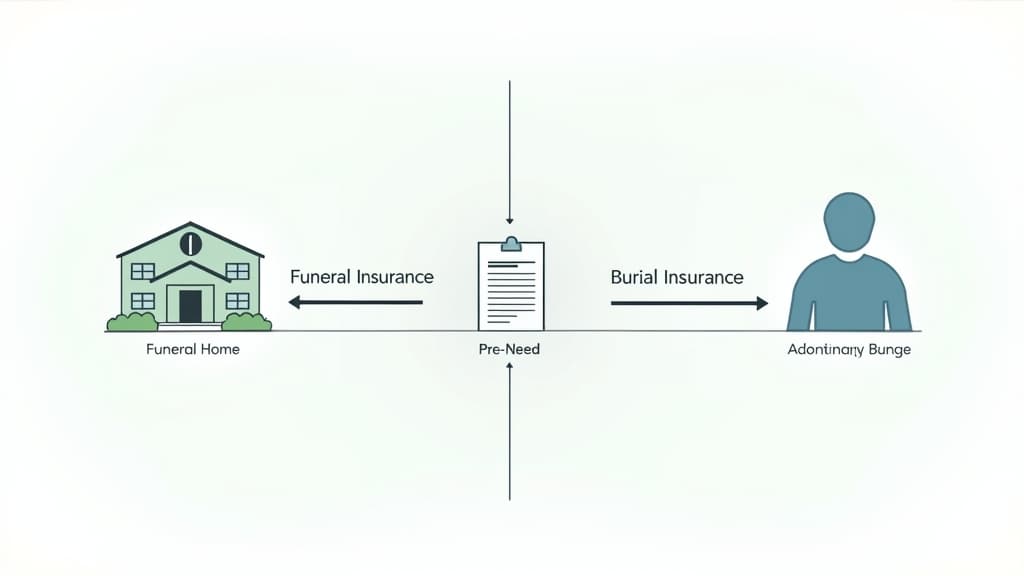

The difference between funeral insurance and burial insurance

Funeral insurance and burial insurance are not the same things, despite how similar they may sound. Funeral insurance usually pays out to the funeral home, while burial insurance usually pays out to the person you choose.

Burial insurance functions similar to a typical whole life insurance policy. There are no rules about what your beneficiaries can do with the money from your life insurance claim once they get it.

While you can express your wishes, the policy makes no provisions for how the money should be used. These plans are quite useful if you want the beneficiaries to have flexibility and independence over how to use their proceeds.

On the other hand, the payout from funeral insurance, which is also called “pre-need life insurance,” is equal to the cost of a prepaid funeral, burial, or cremation.

You’ll get to choose a funeral home, decide on the funeral’s specifics, and then buy the insurance from the funeral director. The funeral home will then fix the cost of the service, so the insurance will always cover the expense, regardless of when you pass away.

Pre-need life insurance can be helpful if you want to ensure that your final wishes are honored and that your family is not left to make funeral arrangements. Inquire about pre-need plans from funeral homes of your choice if this is something that interests you.

Alternatives to funeral insurance

A funeral insurance policy is a viable option if you want to avoid the medical exam or only need a limited amount of coverage. However, there are several other ways to pay for final bills, particularly if you’re in reasonably good health, including term life insurance.

Term life insurance offers short-term protection and may be a more affordable option if you’re aged 50 to 70, healthy, and ready to submit to a medical exam. Term policies often offer lower life insurance rates than other coverage options.

However, even if you can purchase term life insurance to pay for final costs, it might not be the best option. It only lasts for the length of the insurance term, which could be 10 or 20 years, even though you might live longer. Term life insurance is better for the length of a mortgage, the cost of raising children, or the number of years until retirement.

Allocate money for it: Another option is to include a financial provision in your will for your funeral. However, your family might not receive the money on time for the funeral expenses.

Frequently asked questions about funeral insurance

Who can purchase funeral insurance coverage?

Usually, people aged between 50 and 85 can get coverage. One advantage of the funeral policy is that there is no medical examination necessary to be eligible. Even those without insurance coverage or who have a pre-existing disease can typically get a policy, depending on the kind of policy they pursue.

What level of burial insurance do I need?

Consider the precise expenses you want the policy to cover when determining how much funeral insurance to purchase. According to data from the National Funeral Directors Association for 2021, the most recent year available, the median cost of a funeral with viewing and burial is roughly $7,848.

The average cremation expense is roughly $6,971. Even if you plan a grandiose event with flowers, limos, and catered food, your burial insurance coverage should at least cover all of the expenses you have in mind, protecting your family from having to deplete their funds.

Are funeral expenses covered by term life insurance?

Your previous debts and funeral expenses can be paid for out of the payout from your term life insurance policy, depending on what your beneficiaries decide to do with the money. So, you might not need a separate policy for your funeral if you already have a term policy with enough coverage to pay for your last expenses.

Typically, burial insurance is a whole-life policy that is valid until your death. However, your term life insurance will expire if you live past the policy’s term.