🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

Largest Funeral Home Companies in the U.S. (2026) | Memorials.com Info Center

🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee🏬Supersize Online Funeral Retailer🪦1000's of Headstones⚱️Over 10,000 Cremation Urns⚰️Caskets Overnight Delivery🛒Funeral & Memorial Superstore🚚FREE Shipping on ALL Orders👨👩👧👦Helping Families for over 20 Years💰Lowest Price Guarantee

Largest Funeral Home Companies in the U.S.: Who They Are and Why It Matters

The American funeral industry generates roughly $20.8 billion in annual revenue, yet most families never think about who actually owns the funeral home they walk into. That distinction matters more than it might seem. A handful of large corporations now operate thousands of funeral homes and cemeteries across the country, often under the familiar family names those businesses have carried for decades. Understanding who the largest funeral home companies are — and how they differ from independent operators — can help you make a more informed decision when the time comes. For a broader overview of every step involved, see our guide to funeral planning.

This guide profiles the biggest players in the death care industry, explains how consolidation has reshaped the landscape, and explores what it all means for the families these companies serve.

How the Funeral Industry Is Structured

There are approximately 19,000 funeral homes operating in the United States. About 89% of them remain privately owned by families or individuals, many passed down through multiple generations. The remaining share belongs to corporate chains — publicly traded companies, private-equity-backed firms, and regional consolidators that have steadily acquired independent funeral homes since the 1960s.

Industry analysts estimate that the top six funeral operators control between 25% and 30% of all funeral services in North America. The top four alone own between 15% and 20% of all funeral home locations. That means a relatively small number of companies conduct a disproportionately large share of the roughly 3.1 million funerals expected in the U.S. this year.

The consolidation trend has accelerated in recent years. A 2025 survey by the National Funeral Directors Association (NFDA) found that 46% of funeral directors plan to retire within the next five years. When no family successor is available, many directors sell to corporate buyers — the only realistic exit strategy for a business built on personal relationships and local reputation.

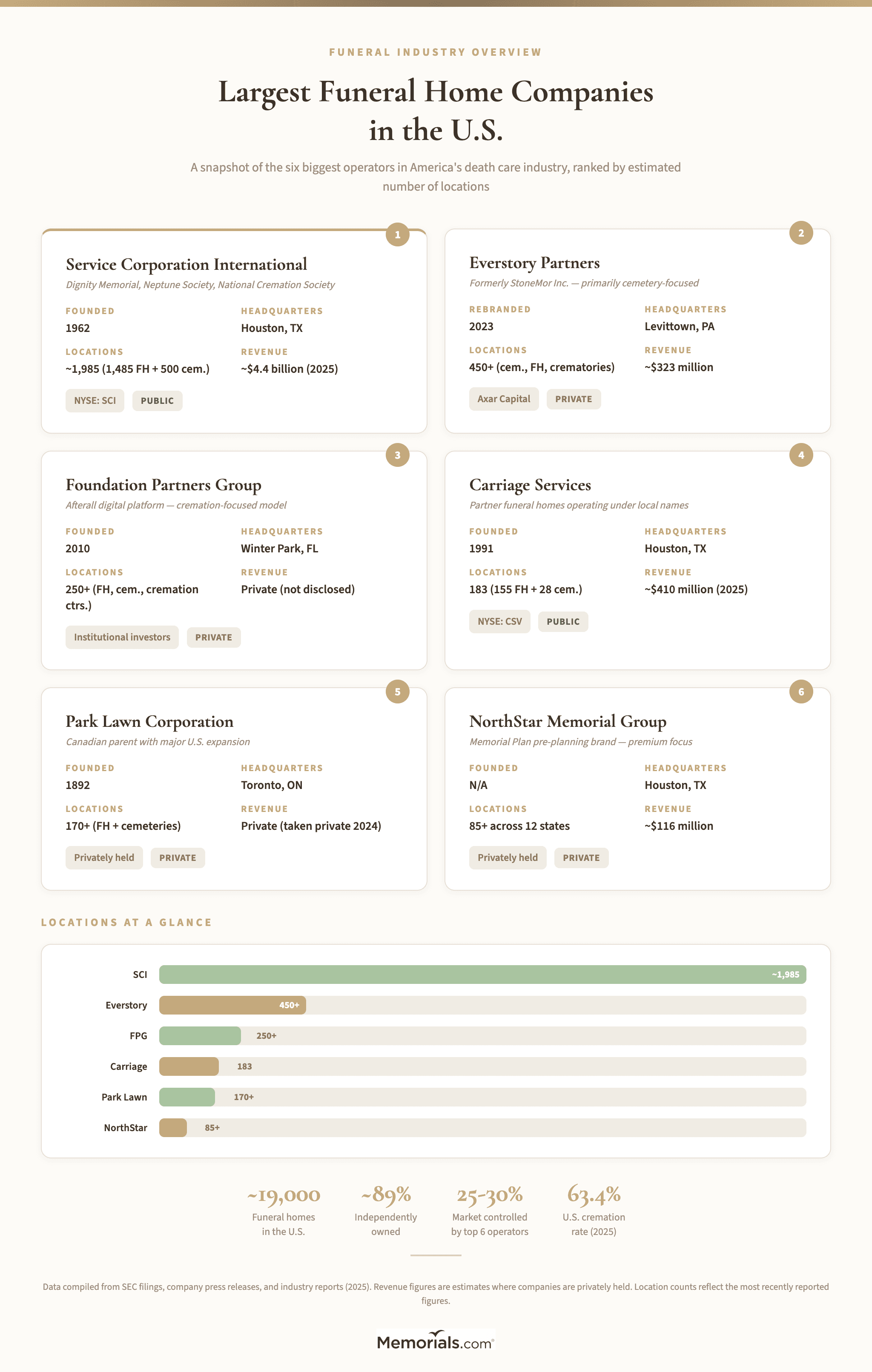

Service Corporation International (SCI) — The Industry Giant

Service Corporation International is by far the largest funeral home company in the United States and the world. Founded by Robert L. Waltrip in Houston, Texas, in 1962, SCI pioneered the "cluster" model of acquiring funeral homes in the same geographic area and sharing back-office resources for cost efficiency.

By the numbers (as of December 31, 2025):

1,485 funeral service locations and 500 cemeteries across 44 states, 8 Canadian provinces, the District of Columbia, and Puerto Rico

Approximately $4.4 billion in annual revenue (full year 2025), with revenue growing 3% year over year

Serves more than 700,000 families per year

Estimated 15–16% market share by revenue

Publicly traded on the NYSE under ticker SCI

SCI's consumer-facing brand is Dignity Memorial, introduced in 1999, though many of its acquired funeral homes still operate under their original family names. The company also operates National Cremation Society, Neptune Society, Advantage Funeral and Cremation Services, and Funeraria del Angel (serving Hispanic communities).

SCI's growth has been defined by acquisitions. It absorbed Alderwoods Group (then the second-largest operator) in 2006 and Stewart Enterprises (the third-largest) in 2013 for $1.4 billion. The Stewart deal required the company to sell 53 funeral homes and 38 cemeteries across 59 markets to satisfy FTC antitrust conditions.

One detail that surprises many families: SCI's pricing tends to run higher than independent funeral homes, even with its lower overhead. Families who want to understand how much funerals cost across different types of providers should compare General Price Lists directly — the FTC's Funeral Rule requires every funeral home to provide one upon request.

Foundation Partners Group — The Cremation-Focused Challenger

Foundation Partners Group (FPG) is the second-largest funeral home provider in the U.S. by number of families served. Founded in 2010 and headquartered in Winter Park, Florida, FPG has taken a markedly different approach from SCI by building its network around cremation-heavy markets.

Key facts:

Over 250 funeral homes, cremation centers, and cemeteries across 21 states

Private company (not publicly traded)

Announced new institutional ownership in August 2025, recapitalizing the business with fresh growth capital

CEO: John D. Smith

Known for its technology-forward approach, including the Afterall digital platform (launched December 2024) that helps families find and arrange services online

FPG's strategy reflects a fundamental shift in the industry. With the national cremation rate reaching 63.4% in 2025 — and projected to exceed 80% by 2045 — the company's cremation-centric model positions it for long-term demand. The question industry observers are watching is whether the thinner margins on cremation services (compared to traditional burial) can sustain a national consolidation strategy over time.

Everstory Partners — The Cemetery Powerhouse

Everstory Partners, formerly known as StoneMor Inc., is the second-largest owner and operator of cemeteries in the United States. The company rebranded in 2023 after being acquired by Axar Capital Management.

Key facts:

Over 450 funeral home and cemetery locations across the U.S. and Puerto Rico

CEO: Lilly Donohue

Headquarters: Levittown, Pennsylvania

Primarily cemetery-focused, with a growing funeral home portfolio

Acquired 83 properties (72 cemeteries, 11 funeral homes) from Park Lawn Corporation in 2023

Everstory's scale is concentrated in cemeteries rather than funeral homes, which distinguishes it from SCI and Foundation Partners. For families evaluating burial options, Everstory-owned cemeteries are common in the eastern United States, though the locations typically operate under their original community names.

Carriage Services — The Publicly Traded Regional Operator

Carriage Services, founded in 1991 and headquartered in Houston, Texas, is the third publicly traded funeral company in the U.S. (alongside SCI and, historically, StoneMor before its privatization).

Key facts:

155 funeral homes in 24 states and 28 cemeteries in 9 states (as of December 31, 2025)

Annual revenue of approximately $410 million

Funeral homes generate about 65% of revenue; cemeteries account for 35%

Publicly traded on the NYSE under ticker CSV

Reported 8% total revenue growth in Q4 2025 and targets up to $450 million in 2026 revenue

Acquired eight funeral homes, one cemetery, and a cremation business in Florida in 2025 for $56.5 million

Carriage Services positions itself around its "Being The Best" philosophy, emphasizing partnership with the funeral directors it acquires rather than imposing a corporate template. The company reported a 3.1% increase in average revenue per funeral contract in 2025, reflecting broader industry trends toward service personalization and higher-value arrangements.

Park Lawn Corporation — Canadian Roots, American Reach

Park Lawn Corporation is a Canadian funeral and cemetery operator that has expanded significantly into the United States. The company was taken private in 2024 in a deal valued at approximately $871 million.

Key facts:

Approximately 170+ funeral home and cemetery locations (after divesting 83 properties to Everstory Partners in 2023)

CEO: Jennifer Hay

Headquarters: Toronto, Ontario, Canada

Continued U.S. expansion in 2025, adding locations in Colorado, New Mexico, Georgia, and Oklahoma

One of the four largest funeral home and cemetery operators in North America by revenue

Park Lawn's strategy has focused on acquiring high-quality funeral homes in markets underserved by the larger chains. The company's failed 2023 bid to acquire Carriage Services signaled its ambitions to grow aggressively in the U.S., and its subsequent property sales to Everstory freed up capital for targeted expansion.

NorthStar Memorial Group — The Premium Operator

NorthStar Memorial Group (NSMG), headquartered in Houston, Texas, operates a smaller but carefully curated portfolio of funeral homes, cemeteries, and crematories.

Key facts:

Over 85 funeral and cemetery locations across 12 states

Annual revenue of approximately $116 million

Private company

Known for its "Memorial Plan" pre-planning brand and premium service focus

NorthStar tends to acquire higher-end properties in desirable markets rather than pursuing volume-based consolidation. The company has expanded in Florida, Texas, California, and Hawaii, among other states.

Other Notable Funeral Home Corporations

Beyond the major operators, several other companies play significant roles in the death care landscape:

Milestone Funeral Partners, backed by Rosewood Private Investments (acquired in 2024), has consolidated aggressively in the northeastern United States. The company owns 77 funeral homes throughout New England and New York. In some counties, Milestone owns 20% or more of all funeral home locations — a concentration level that raises questions about local competition and pricing.

Newcomer Funeral Service Group operates funeral homes across several states with a focus on value-oriented, transparent pricing. Newcomer has built its brand specifically around affordability, positioning itself as a lower-cost alternative in markets dominated by higher-priced corporate operators.

SCI-affiliated brands worth knowing include Neptune Society and National Cremation Society, both of which operate as separate cremation-focused brands under the SCI corporate umbrella. These brands target families seeking direct cremation and tend to operate at lower price points than Dignity Memorial locations, though they are ultimately owned by the same parent company.

Why Consolidation Is Accelerating

Several forces are driving funeral home consolidation in the mid-2020s.

The retirement wave. Nearly half of all funeral directors surveyed by the NFDA plan to retire by 2030. Funeral homes are intensely personal businesses — when the family name on the building retires, the business often sells. Corporate acquirers are the most frequent buyers because they can pay premium prices, retain existing staff, and keep the familiar brand intact.

The cremation shift. The U.S. cremation rate stood at 63.4% in 2025, more than double the burial rate of 31.6%. Every state is projected to surpass 50% cremation by 2035. Cremation services generally generate less revenue per case than traditional funerals, which puts pressure on smaller independent operators who lack the volume to make up the difference.

Private equity interest. Beyond the established funeral corporations, private equity firms have entered the death care space aggressively. Firms see funeral homes as recession-resistant assets with stable demand tied to demographics rather than economic cycles. The real estate value of funeral home and cemetery properties — often located on prime land in established neighborhoods — adds another layer of investment appeal.

The baby boomer effect. The U.S. death rate is rising as the baby boomer generation ages. Approximately 3.1 million deaths are projected for 2026, a number that will continue climbing for decades. Investors view this as a rare combination of demographic certainty and recession resistance.

What Consolidation Means for Families

For families in the middle of planning a funeral, the corporate-versus-independent distinction has practical implications.

Pricing. Corporate funeral homes often charge more than independent operators for comparable services. Research has consistently found that SCI-operated locations, in particular, tend to price above the market average despite their economies of scale. The FTC's Funeral Rule gives every family the right to a General Price List — use it. Request price lists from multiple providers before committing.

Brand transparency. Many corporate-owned funeral homes continue operating under their original family names. There is no requirement to disclose corporate ownership prominently. If knowing who owns the funeral home matters to you, ask directly or check state licensing records.

Service consistency vs. personal touch. Corporate chains often provide consistent facilities, professional staff, and standardized processes. Independent funeral homes may offer more personalized service, flexibility in arrangements, and deeper community roots. Neither model is inherently better — what matters is which approach fits your family's needs and values.

Pre-need sales pressure. Large funeral companies, particularly SCI, generate substantial revenue from preneed contracts — funeral arrangements purchased in advance. Preneed planning can be a smart financial move, but families should carefully compare preneed prices with at-need pricing and understand cancellation terms before signing.

Using a funeral planning checklist can help your family organize decisions and compare providers systematically, whether you choose a corporate or independent funeral home.

How to Research a Funeral Home's Ownership

Before choosing a provider, consider these steps:

Ask directly. The simplest approach. Call the funeral home and ask whether it is independently owned or part of a corporate group.

Check state licensing records. Most states maintain public databases of licensed funeral establishments that include ownership information. Some states, like Massachusetts, require funeral homes to disclose all entities with an ownership stake.

Compare General Price Lists. The FTC requires funeral homes to provide itemized pricing upon request. Comparing lists from multiple providers — both corporate and independent — reveals how pricing differs in your local market.

Look for the brand. Funeral homes operating under the Dignity Memorial, Neptune Society, or National Cremation Society brand are SCI-owned. Foundation Partners Group properties can be identified through the Afterall platform. Carriage Services locations are listed on the company's investor website.

Read reviews carefully. Online reviews can reveal service quality, but keep in mind that corporate-owned funeral homes operating under family names may receive reviews that don't distinguish between corporate and pre-acquisition management.

The Role of Independent Funeral Homes

Despite consolidation, independent funeral homes remain the backbone of the American death care industry. Families seeking alternatives to traditional funerals — green burials, home funerals, celebration-of-life events, or culturally specific practices — often find independent operators more willing to accommodate non-standard requests.

Independent funeral homes also tend to be more deeply embedded in their communities. They sponsor local events, maintain relationships with area clergy and hospitals, and often provide services that extend well beyond the funeral itself. For families whose faith traditions carry specific requirements — such as those navigating Catholic funeral planning — an independent funeral home with experience in those traditions can offer guidance that a corporate protocol might not cover as naturally.

Organizations like the National Funeral Directors Association (NFDA) and Selected Independent Funeral Homes maintain membership directories that can help families identify independently owned providers in their area.

The Funeral Industry's Future

The funeral industry is in the midst of a structural transformation. Cremation has moved from a minority choice to the clear majority preference, and it will likely account for 80% of all dispositions by 2045. That shift is reshaping everything from facility design to revenue models to how families think about memorialization.

For the largest funeral home companies, the path forward involves scale, technology, and diversification. SCI's $16 billion preneed backlog provides a revenue cushion that few competitors can match. Foundation Partners Group's digital-first approach targets families who increasingly expect to arrange services online. Carriage Services is returning to acquisitions after a period of debt reduction.

For families, the most important takeaway is this: corporate ownership is neither inherently good nor bad. What matters is the quality of care, the transparency of pricing, and whether the funeral home's values align with your own. Ask questions, compare costs, and choose the provider that feels right — regardless of who signs the checks.

Frequently Asked Questions

Who is the largest funeral home company in the United States?

Service Corporation International (SCI) is the largest funeral home company in the U.S. and the world. The company operates approximately 1,485 funeral homes and 500 cemeteries across 44 states, serving over 700,000 families per year. Its consumer-facing brand is Dignity Memorial.

How can I tell if a funeral home is corporate-owned?

Many corporate-owned funeral homes operate under their original family names, so ownership is not always obvious. You can ask the funeral home directly, check state licensing records, or look for brand affiliations such as Dignity Memorial (SCI), National Cremation Society (SCI), or Afterall (Foundation Partners Group).

Are corporate funeral homes more expensive than independent ones?

Generally, yes. Research has found that corporate-owned funeral homes — particularly those operated by SCI — tend to charge more than independent funeral homes for comparable services. The FTC's Funeral Rule requires all providers to furnish a General Price List upon request, making direct comparison straightforward.

How many funeral homes are there in the United States?

There are approximately 19,000 funeral homes in the United States. Roughly 89% are independently owned by families or individuals. The remaining share is owned by corporate chains, private-equity-backed firms, and regional consolidators.

Is the funeral industry growing?

Yes. The U.S. funeral services market is valued at approximately $20.8 billion in 2025 and is projected to grow steadily as the baby boomer generation ages and the annual death count rises. The industry is also diversifying as cremation, green burial, and digital memorialization expand the range of services families seek.